The Fayetteville Shale was the second shale gas play to succeed. The Barnett Shale proved the technology to work. And in doing so, opened a Pandora’s Box of horizontal shale plays dependent upon the slick water frack; or early in the play, nitrogen and carbon dioxide fracks. Some failed while others succeeded spectacularly. The Caney, a shale situated between the Fayetteville and the Barnett geologically, was a dud. But the Haynesville and Fayetteville suddenly added a huge influx of natural gas to the supply. That proved incentives to drill other areas, including the Marcellus Shale and Utica Shale of the Northeast.

The problem then became price as surplus led to lower prices, prices so low that wells were often uneconomic despite producing a lot of gas. But the nail in the coffin for the dry shale basins like the Fayetteville was oil. At first, drillers didn’t believe they could make any oil whatsoever from a shale well. But that proved to be wrong.

The Woodford, Bakken, Haynesville, Niobrara, and other oily shales proved to be able to produce a huge flush of oil with a lot of natural gas to boot. The oil was needed far more than the gas. Then someone figured out that any tight reservoir, shale, sand or lime, would respond to large fracks and long horizontal laterals. The race was on.

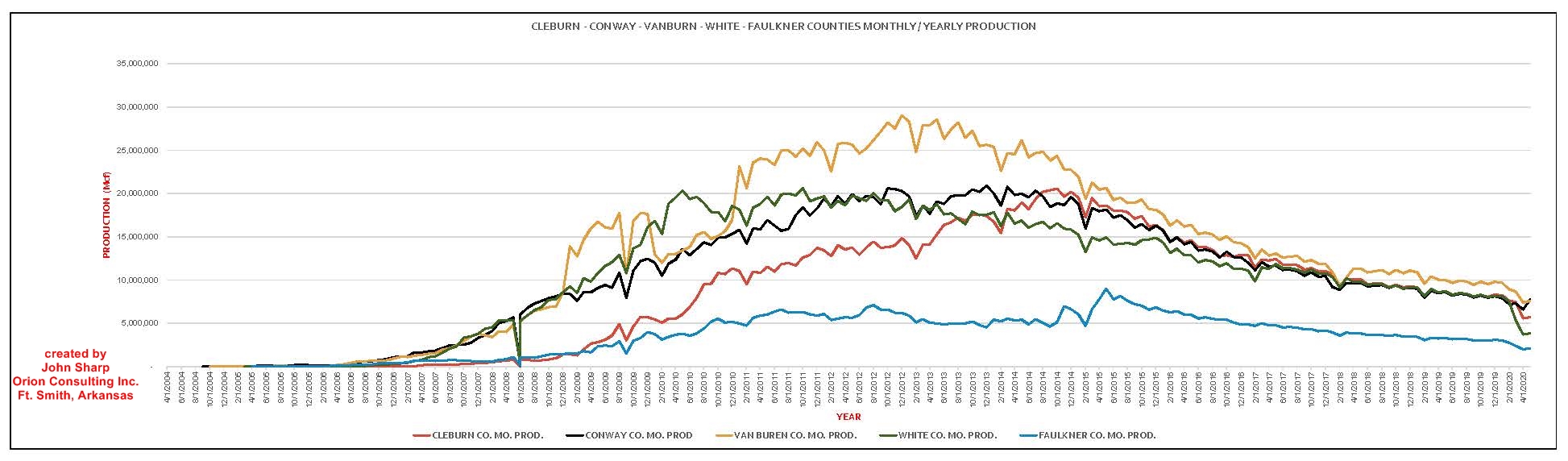

But rapidly the pipelines bulged with unwanted gas. Gas prices fell like a rock and have never recovered since 2014 to anything near an economic price. Drillers begged regulators to let them flare the gas, simply burn it off to get to the oil. That left the Fayetteville and Barnett in the dust. The chart below shows the very rise and fall of the Fayetteville shale. The basin is dying and production is tiny percentage of its peak. No new wells have been drilled for several years. No leases have been taken. And no one is buying mineral rights. The intrinsic value of the gas will have to wait until the price is sufficient to justify additional drilling. And that may be decades.

Meanwhile, these “oil wells” produced oil for a while then rapidly became gas only wells. Once reservoir pressure is depleted, the oil cannot find the borehole and only the smallest molecules of natural gas or “liquids” (mostly ethane or propane) can reach the borehole and be produced. So the glut of natural gas remains and at $1 to perhaps $1.50/MCF is below the price necessary to cash flow a well profitably. The glut got so bad in West Texas that the natural gas price fell to a single penny. Then this spring (2020) oil futures crashed into negative territory finally bringing a halt to the idea that the Permian Basin was some sort of money machine. Dozens of oil operators and hundreds of service companies have closed their doors or filed bankruptcy, including Chesapeake Energy, one of the earliest pioneers in the shale boom. It’s no surprise to old timers like me who has seen boom and bust all before.

My appreciation to John Sharp (Orion Consulting, Inc.) of Fort Smith, Arkansas for the graph used below.

Production curves of Select Counties in the Fayetteville Shale