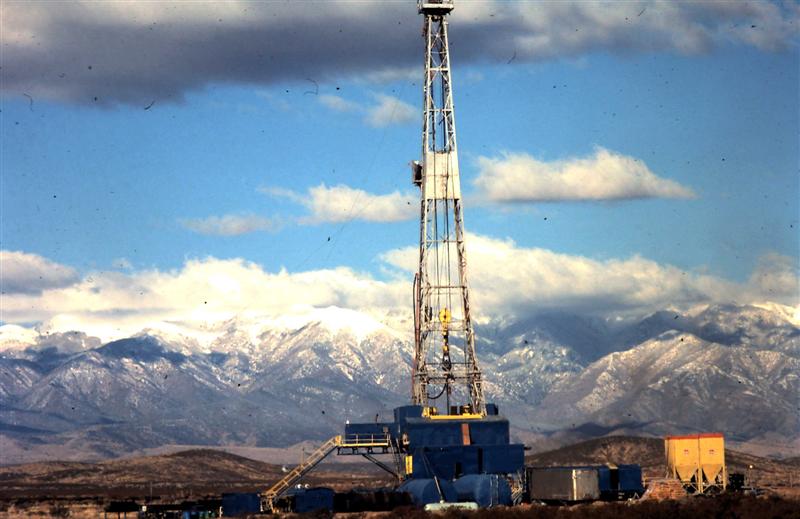

The notion that the pain will end soon, and prices will not so much stabilize as to see costs go down is a pipe dream floated by true “believers” not serious students of the oil business. There is an idea that you will see the cost of frac’cing and drilling go down to meet the prices imposed upon oil by Wall Street’s energy traders. But it is obvious that banks are laying back reserves to cover losses they expect from failing oil companies. There is no lender of last resort for oil. It has to crash. It is taking down company after company as we speak.

This week people still think the drillers are finding ever increasing reserves. In truth, they are merely developing the thousands of wells that had not been completed. As those diminish, reserves will stabilize and start to fall. The current fleet of rigs are not laying down as many but half the rigs are mothballed.

So the process of completing those wells and seeing their reserves fall (50% will be produced in the first two years) while the remaining reserves will take from six to perhaps 30 years to be produced. So it is not an overnight process. When we reach that stable point – perhaps in 2016 or 2017, then prices will probably not rebound much unless we are allowed to export oil. But costs while down, are going to remain high. The shale revolution forgot to tell people that the process is costly and is much higher than most people realize. Some people in the business have privately said that they have yet to recoup their investment in the Mississippian or in the Niobrara. The Bakken, for smaller operators, probably even less so. And even Continental Resources may be “going down” either to fold up, downsize and sell off assets at fire sale prices, or be acquired by the likes of ConocoPhillips or ExxonMobil.

The drillers have been laid off. The less than ideal worker, or those who are greenhorns are gone. And now the junior staffers at the companies – engineers, geologists, and others – well, they are going day by day as companies close satellite offices, and shorten staff. And we recycle the joke about the desperate engineer applying for a job in McDonalds and being turned down with, “Sorry, all our engineers have master’s degrees.”

My beautiful picture